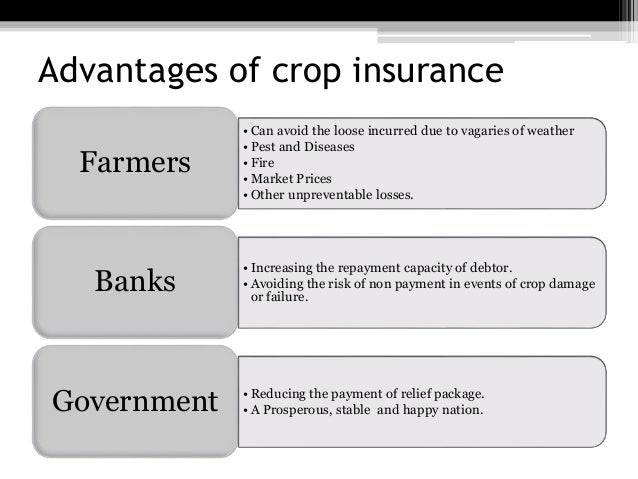

Crop Insurance

- Refers to insurance services brought by farmers against loss or damage to growing crops.

- Damages can be due to natural disasters such as drought, hail, floods, or either due to decline in prices of the agriculture commodity.

History of Crop Insurance in India

- As far back as 1915 in the pre-independence era, J.S. Chakravarthi had proposed a rain insurance scheme for the farmers with view to insuring them against drought. His scheme was based on, what is referred to today as the ‘Area Approach’.

- Apart from this, certain princely states like Madras, Dewas, and Baroda, also made attempts to introduce crop insurance relief in various forms, but with little success.

- After independence, the first crop insurance program was introduced in 1972-73 by LIC on Cotton in Gujarat.

- Later in 1972, the newly set up General Insurance Corporation (GIC) took over the experimental scheme and subsequently widened the coverage of crops as well as area of implementation. This experimental scheme was based on ‘Individual Approach’.

- It was realized that crop insurance programmes based on the individual farm approach would not be viable in India.

- Professor V. M. Dandekar (Father of Crop Insurance in India) suggested an alternate ‘Homogeneous Area Approach’. Based on this approach, the General Insurance Corporation of India (GIC) introduced a Pilot Crop Insurance Scheme from 1979.

- Based on the learning from Pilot Crop Insurance Scheme, the Comprehensive Crop Insurance Scheme was introduced in 1985 by the Government of India. The CCIS was implemented on Homogeneous Area Approach. All crop loans given for notified crops in notified areas were compulsorily covered under the CCIS.

- The CCIS was eventually discontinued after Kharif 1999, to be replaced by the improved and expanded National Agriculture Insurance Scheme (NAIS).

- Later “National Crop Insurance Programme” was launched in 2013 by merging three schemes viz. Modified National Agricultural insurance Scheme (MNAIS), Weather Based Crop insurance Scheme (WBCIS) and Coconut Palm Insurance Scheme (CPIS).

- Since 2016, Pradhan Mantri Fasal Bima Yojana is being implemented by replacing MNAIS and CPIS.

- But WBCIS is still working along with PMFBY.

Crop Insurance Schemes

Why it is difficult to design

- The risk of crop loss has a significant systemic component; and

- Ex ante risk assessment and ex post loss assessment for individual farmers are costly.

Crop insurance is mandatory for

- farmers who have taken short-term crop loan (loanee farmers).

But Crop Insurance is voluntary for

- all other farmers (non-loanee farmers).

The premium of crop insurance is

- Is deducted from the loan amount for loanee farmers, and claim, if any, is adjusted against the loan amount.

- The non-loanee farmers, pay premium from their pocket, and receive the claim amount if crop loss is recognised.

Coverage of crop insurance (according to Govt):

- around 26% farmers have been covered in 2017 so far.

Reasons behind the low demand for crop insurance in India

- In India, demand for crop insurance is highly price-sensitive.

- Even a small change in premium rates leads to wide shifts in demand.

- PMFBY, with its attractive premium, is expected to be a hit.

- Poor awareness.

- An overwhelming majority (60% farmers) lack awareness about crop insurance schemes (NSSO)

- Delay in settlement of claims.

- Lengthy and complex system of claim settlement discourages farmers from insuring their crops.

- Mandatory only for loanee farmers

- Thus, PSBs do not have any incentive to sell it to non-loanee farmers.

Livestock Insurance

The Livestock Insurance Scheme:

- Is centrally sponsored scheme

- Implemented on a pilot basis during 2005-08 in 100 selected districts

- Presently being implemented in all districts of the country (since 2014) as a sub-mission under the National Livestock Mission

Under the scheme

- The animals

- Indigenous / crossbred milch animals

- Pack animals (Horses, Donkey, Mules, Camels, Ponies and Cattle/Buffalo Male)

- and Other Livestock (Goat, Sheep, Pigs, Rabbit, Yak and Mithun etc.)

- The insurance:

- Done at their current market price

- Premium subsidy of 50% is borne entirely by centre

- Twin objectives are to:

- Protect incomes

- Popularize livestock insurance (ultimate aim – qualitative improvement in livestock and their products)

CAG report on Agriculture insurance in India

- CAG audit report of centre’s crop insurance schemes has highlighted gaps in their implementation.

- Two schemes that were audited: From Kharif 2011 to Rabi 2015-16

- Modified National Agriculture Insurance Scheme ( MNAIS )

- National Crop Insurance Programme ( NCIP )

- The present Pradhan Mantri Fasal Bima Yojana has not been scrutinised by the CAG.

- It came in Kharif 2016.

Problems highlighted by CAG in Agri-insurance in India

- Delayed payments by state government.

- Agriculture Insurance Company Of India Ltd. ( AIC ) failed to follow due to protocols in verification of claims by private insurance companies before releasing funds to them.

- Difficulty in cross checking

- Missing records of beneficiaries

- The low inclusion of Small and Marginal farmers

- Low coverage of non-loanee farmers.

- Lack of Awareness

Pradhan Mantri Fasal Bima Yojana (PMFBY)

- Started in the Kharif season of 2016

- To reduce the burden of crop insurance on farmers.

- In line with ‘One Nation – One Scheme’ theme.

- Replaced the National Agricultural Insurance Scheme (NAIS) and Modified National Agricultural Insurance Scheme (MNAIS).

- The Weather-Based Crop Insurance Scheme (WBCIS) remains in place, though its premium rates have been made the same as in PMFBY.

- State governments to decide whether they want PMFBY, WBCIS or both in their states.

- It incorporates the best features of all previous schemes and at the same time, all previous shortcomings/weaknesses have been addressed.

How is PMFBY different

- Lowest premium for farmers

-

-

- in the history of Independent India

- kept at a maximum of 1.5% for Rabi, 2% for Kharif and 5% for annual horticultural/commercial crops

-

- Uncapped premium would ensure farmers get a higher claim

-

-

- ≥25% of the claim is settled directly through farmers’ bank account

- previous schemes had higher + capped premium

-

- The scheme is open to all farmers irrespective of whether they are loanees or not

-

-

- previously, loanee farmers were mandated to take crop insurance

-

- Covers localised losses due to floods

-

-

- Only hailstorm and landslide were covered in previous schemes.

-

- Post-harvest loss

-

-

- Previous schemes covered only coastal areas for cyclones.

- PMFBY covers all-India for both cyclonic and unseasonal rains.

-

- Use of modern tech for quicker assessment and claim settlement

-

-

- PMFBY makes it mandatory – remote sensing, smartphones etc

- Previous schemes only relied on Crop Cutting Experiment (CCE) data instead

- Collecting this data and processing of claims delayed settlement

-

- Awareness generation (AG)

-

- Previous schemes did not focus on AG; therefore insurance adoption remained low

- PMFBY targets at least 50% coverage through greater AG

Successes of PMFBY

- In the very first Kharif season (2016)

-

- The area under coverage increased by 38% (vs. 2015)

- The number of farmers covered increased by 47% (vs. 2015)

- Sum insured (per ha) increased by 51% (vs. 2015)

- The number of non-loanee farmers opting for PMFBY increased by 23%, driven primarily by Maharashtra.

- Increase in risk coverage against non-preventable natural risks from pre-sowing to post-harvest losses

Challenges / Loopholes

- Settling claims

-

-

- Slow submitting yield data by states to the insurance companies.

- The lackadaisical attitude of state agencies causes painful delays.

- Farmers still to get over Rs 5,600 crore worth of estimated claims from the 2016 kharif season

-

- Assessing crop losses

- Modern tech not used to the fullest, despite being mandatory causing huge delays in assessment and reporting

- The states are also slow in conducting village-level crop-cutting experiments

- No direct connection with the farmers

- Everything from damage assessment to claim settlement by govt and insurance companies.

- Therefore farmers have no role.

- The premiums are collected and passed on by the banks that extend loans to the farmers.

- “More as loan insurance than as crop insurance”.

Conclusion on PMFBY

- PMFBY has made appreciable progress in terms of coverage

- But it has failed in timely settlement of claims

- If the PMFBY has to succeed farmers must have a bigger stake in its functioning

- Use modern tech in crop assessment and reporting

- Modern tech is crucial for timely claim settlement

- Link the insurance database with Core Banking Solution (CBS) so as to keep farmers apprised of premium deductions and claim receipt

- Centre should take over the entire premium subsidy burden.

- Ensure social audit

- Cross check by various authorities and stakeholders