Financial Inclusion in India and Its Challenges

RBI’s Financial Stability Report (FSR) 2024 and Rising Household Debt

From UPSC perspective, the following things are important :

Prelims level: Financial Stability Report

Why in the News?

The Reserve Bank of India (RBI) Financial Stability Report (FSR), 2024 has highlighted an increasing household debt burden and a concerning rise in consumption-based borrowing.

About Financial Stability Report (FSR):

- The FSR is published biannually (June & December) by the RBI.

- It reflects the collective assessment of the Sub-Committee of the Financial Stability and Development Council (FSDC – headed by the Governor of RBI) on risks to financial stability and the resilience of the financial system.

- The Report also discusses issues relating to the development and regulation of the financial sector.

Key Highlights of the Financial Stability Report (FSR) 2024:

- Rising Household Debt-to-GDP Ratio:

-

- Household debt-to-GDP ratio: 36.6% (June 2021) → 42.9% (June 2024).

- Household assets declined: 110.4% (June 2021) → 108.3% (March 2024), indicating more borrowing for consumption.

- Credit Growth Trends:

-

- Total credit growth (March 2024): 15.4% YoY.

- Prime & Super-Prime borrowers: 66% of total loans, reducing risky lending.

- Super-prime borrowers mainly borrow for asset creation, while sub-prime borrowers rely on loans for consumption.

- Rising Unsecured Loans & Financial Stress:

-

- 50% of sub-prime loans are for consumption; 64% of super-prime loans are for asset creation.

- Credit card delinquencies: 1.8% (Sept 2023) → 2.4% (Sept 2024).

- Personal loan defaults: 3.2% (Sept 2023) → 3.9% (Sept 2024).

- Low-income households rely more on credit cards & personal loans than secured loans.

- RBI’s Measures to Curb Consumer Borrowing:

-

- September 2023: RBI raised risk weights on unsecured loans, slowing credit expansion.

- Auto loan growth fell: 18.2% (March 2023) → 14.5% (March 2024) due to tighter lending norms.

- Consumption Loans & Economic Impact:

-

- More borrowing for consumption, less for housing, education, or business investment.

- Rising debt repayment reduces spending, weakening GDP growth.

- NPA Risks from Consumer Credit:

-

- Unsecured loans growing faster, raising default risks.

- Half of borrowers with credit card/personal loans also have home/auto loans—defaulting on one triggers loan classification as NPA.

- Fintech’s Role in Rising Debt:

-

- Digital lending & BNPL schemes enable easy credit but increase financial vulnerability.

- Regulatory oversight needed to prevent excessive debt accumulation.

PYQ:[2022] In India, which one of the following is responsible for maintaining price stability by controlling inflation? (a) Department of Economic Affairs, Ministry of Finance (b) Financial Stability and Development Council (FSDC) (c) NITI Aayog (d) Reserve Bank of India |

Get an IAS/IPS ranker as your 1: 1 personal mentor for UPSC 2024

Financial Inclusion in India and Its Challenges

Over 70% Farmers still use Cash to sell their Produce

From UPSC perspective, the following things are important :

Prelims level: Read the attached story

Why in the News?

The Reserve Bank of India (RBI) survey on agricultural transactions reveals that cash remains the primary mode of payment among farmers, although digital payments are gradually increasing. Despite the rise of Unified Payments Interface (UPI) and mobile banking, over 70% of Indian farmers still rely on cash for selling their produce.

Key Findings of the RBI Survey

- In 2019, 88% of farmers used cash for transactions. By 2022, this figure dropped to 79% and further declined to 72% in 2024.

- However, this transition is slow compared to other sectors of the economy.

- The share of farmers using electronic payments has increased from 8% in 2019 to 18% in 2024.

- Among traders, the adoption of digital payments has been faster, rising from 8% in 2019 to 31% in 2024.

- Among retailers, the usage of electronic payments increased from 3% in 2019 to 22% in 2024.

Reasons behind low Digital Adoption

- 55% of farmers rely on traders to determine market prices, up from 47% in 2019. 47% depend on fellow farmers, while fewer than 10% use apps or websites to check market rates.

- Despite the growth of agri-tech platforms, most farmers still depend on word-of-mouth rather than digital sources for price information.

- Multiple intermediaries in the supply chain reduce farmers’ share in the final consumer price.

- 64% of farmers reported crop damage during the 2023-24 rabi season. Unseasonal rainfall was cited as the top reason (37%), followed by heatwaves (30%).

- As a result, 90% of farmers consider weather forecasts as the most important factor in crop-sowing/ harvesting decisions.

PYQ:[2010] With reference to India, consider the following:

Which of the above can be considered as steps taken to achieve the “financial inclusion” in India? (a) 1 and 2 only [2016] Pradhan Mantri Jan Dhan Yojana (PMJDY) is necessary for bringing unbanked to the institutional finance fold. Do you agree with this for financial inclusion of the poorer section of the Indian society? Give arguments to justify your opinion. |

Get an IAS/IPS ranker as your 1: 1 personal mentor for UPSC 2024

Financial Inclusion in India and Its Challenges

NABARD Survey on Rural Financial Inclusion

From UPSC perspective, the following things are important :

Prelims level: NABARD, NAFIS Survey

Why in the News?

The National Bank for Agriculture and Rural Development (NABARD) has published findings from its second All India Rural Financial Inclusion Survey (NAFIS) 2021-22.

About the NAFIS 2021-22

|

Key Highlights from NAFIS 2021-22:

| Details | |

| 1. Increase in Average Monthly Income | • Average monthly income increased by 57.6% from Rs. 8,059 in 2016-17 to Rs. 12,698 in 2021-22, indicating a nominal CAGR of 9.5%. • Agricultural households earned slightly more, with an average income of Rs. 13,661, compared to Rs. 11,438 for non-agricultural households. • Salaried employment was the largest income source for all households, accounting for approximately 37% of total income. • For agricultural households, cultivation was the main income source, contributing about one-third of their monthly earnings. • For non-agricultural households, government/private services contributed 57% of the total household income. |

| 2. Rise in Average Monthly Expenditure | • Average monthly expenditure increased from Rs. 6,646 in 2016-17 to Rs. 11,262 in 2021-22. • Agricultural households had higher expenditure at Rs. 11,710, compared to Rs. 10,675 for non-agricultural households. • In states like Goa and Jammu & Kashmir, monthly household expenditure exceeded Rs. 17,000. • Overall, agricultural households demonstrated both higher income and expenditure levels than non-agricultural households. |

| 3. Increase in Financial Savings | • Annual average financial savings rose to Rs. 13,209 in 2021-22 from Rs. 9,104 in 2016-17. • 66% of households reported saving money in 2021-22, up from 50.6% in 2016-17. • 71% of agricultural households reported savings, compared to 58% of non-agricultural households. • States with 70% or more households saving money include Uttarakhand (93%), Uttar Pradesh (84%), and Jharkhand (83%). • States with less than half of households reporting savings are Goa (29%), Kerala (35%), Mizoram (35%), Gujarat (37%), Maharashtra (40%), and Tripura (46%). |

| 4. Kisan Credit Card (KCC) Usage | • 44% of agricultural households possessed a valid Kisan Credit Card (KCC). • Among those with land holdings greater than 0.4 hectares or who had taken agricultural loans from banks in the past year, 77% had a valid KCC. |

| 5. Insurance Coverage | • Households with at least one member covered by any form of insurance increased from 25.5% in 2016-17 to 80.3% in 2021-22. • 80.3% means that four out of every five households had at least one insured member. • Agricultural households had higher insurance coverage than non-agricultural households by about 13 percentage points. • Vehicle insurance was the most prevalent, with 55% of households covered. • Life insurance coverage extended to 24% of households, with agricultural households showing slightly higher penetration (26%) compared to non-agricultural ones (20%). |

| 6. Pension Coverage | • Households with at least one member receiving any form of pension increased from 18.9% in 2016-17 to 23.5% in 2021-22. • Overall, 54% of households with at least one member over 60 years old reported receiving a pension. • Pensions included old age, family, retirement, or disability pensions, highlighting their importance in supporting elderly members of society. |

| 7. Financial Literacy | • Respondents demonstrating good financial literacy increased from 33.9% in 2016-17 to 51.3% in 2021-22, a rise of 17% points. • Individuals exhibiting sound financial behavior increased from 56.4% to 72.8% during the same period. • When assessed on financial knowledge, 58% of rural respondents and 66% of semi-urban respondents answered all questions correctly. |

Key aspects that contribute to Rural Empowerment

- The survey shows significant progress in rural financial inclusion since the first survey in 2016-17.

- Rural households have seen improvements in income, savings, insurance coverage, and financial literacy.

- Government schemes like Pradhan Mantri Kisan Samman Nidhi, MGNREGS, and PMAY-G have contributed to the improvement in the lives of rural people.

PYQ:[2015] Pradhan Mantri Jan-Dhan Yojana was launched by the Prime Minister of India Narendra Modi on 28 August 2014. What is the main objective of the scheme? (a) To provide housing loan to poor people at cheaper interest rates (b) To promote women’s Self Help Groups in backward areas (c) To promote financial inclusion in the country (d) To provide financial help to marginalised communities |

Get an IAS/IPS ranker as your 1: 1 personal mentor for UPSC 2024

Financial Inclusion in India and Its Challenges

Is it time for India to introduce a Universal Basic Income?

From UPSC perspective, the following things are important :

Mains level: Impact of automation on the Indian economy;

Why in the News?

The rise in jobless growth, driven by automation and AI, has led to growing inequality, prompting discussions on implementing Universal Basic Income (UBI) in many countries.

What does the ILO say on Inflation and unemployment in India?

- The ILO reports that 83% of the unemployed population in India are youth, due to the rapidly changing economy influenced by automation and AI.

- This trend has exacerbated income inequality, with a 1.6% drop in global labour income share between 2004 and 2024, significantly affecting developing nations like India.

- The report indicates that persistent inflation and geopolitical tensions have led to aggressive monetary policies, which could further strain the labor market.

- The ILO anticipates a slight increase in global unemployment in 2024, reflecting ongoing structural issues in labor markets.

What will be its implications on Indian growth and development?

- Social Implications: Falling living standards and weak productivity due to automation could lead to greater inequality, undermining social justice efforts in India.

- The ILO suggests that increasing unemployment and inflation could result in social unrest and political instability without effective social safety nets.

- Political Implications: It makes it difficult for the decision making and governance due to the drop in global labour income, prompting India to increase budget allocations for welfare programs.

- Economic Implications: The emphasis on generating employment in labor-intensive sectors is crucial. The government policies should prioritize job creation to counteract the effects of automation and ensure that growth benefits a broader segment of the population.

What are the safety nets for India?

- Cash Transfer Schemes: Programs targeting farmers and women, as well as cash transfers for unemployed youth, represent existing safety nets that provide some level of income support.

- Employment Guarantee Schemes: Initiatives like the Mahatma Gandhi National Rural Employment Guarantee Act (MGNREGA) aim to provide employment and income security to rural households, although funding and implementation have faced challenges.

- Universal Basic Social Safety Nets: Experts suggest that rather than a full UBI, India should focus on enhancing existing social safety nets to ensure they are more universal and effective in addressing the needs of the unemployed and underemployed populations.

Get an IAS/IPS ranker as your 1: 1 personal mentor for UPSC 2024

Financial Inclusion in India and Its Challenges

[pib] 10 Years of Jan Dhan Scheme

From UPSC perspective, the following things are important :

Prelims level: Pradhan Mantri Jan Dhan Yojana (PMJDY)

Why in the News?

PM Modi launched the Pradhan Mantri Jan Dhan Yojana (PMJDY) on 28th August 2014. It has now completed a decade of successful implementation.

About PMJDY

| Details | |

| Objective | • Banking the Unbanked: Open basic savings bank deposit (BSBD) accounts with minimal paperwork, relaxed KYC, e-KYC, account opening in camp mode, zero balance & zero charges. • Securing the Unsecured: Issue Indigenous Debit cards with free accident insurance coverage of ₹2 lakh. • Funding the Unfunded: Provide micro-insurance, overdraft, micro-pension, and micro-credit facilities. |

| Initial Features | • Universal Access to Banking Services: Access through branches and BCs. • Basic Savings Bank Accounts: With an overdraft facility of up to ₹10,000 for every eligible adult. • Financial Literacy Program: Promote savings and credit usage. • Insurance: Accident cover up to ₹1 lakh and life cover of ₹30,000 for accounts opened between Aug 2014 to Jan 2015. • Pension Scheme: For the unorganized sector. • Creation of Credit Guarantee Fund. |

| Key Provisions | • Inter-operability: Through RuPay debit card or Aadhaar-enabled Payment System (AePS). • Fixed-point Business Correspondents. • Simplified KYC / e-KYC. |

| Extension and New Features (Post-2018) | • Focus Shift: From ‘Every Household’ to ‘Every Unbanked Adult’. • RuPay Card Insurance: Increased accidental insurance cover to ₹2 lakh for new accounts. • Overdraft Facilities Enhanced: Limit doubled from ₹5,000 to ₹10,000; up to ₹2,000 without conditions. • Increase in upper age limit for OD: From 60 to 65 years. |

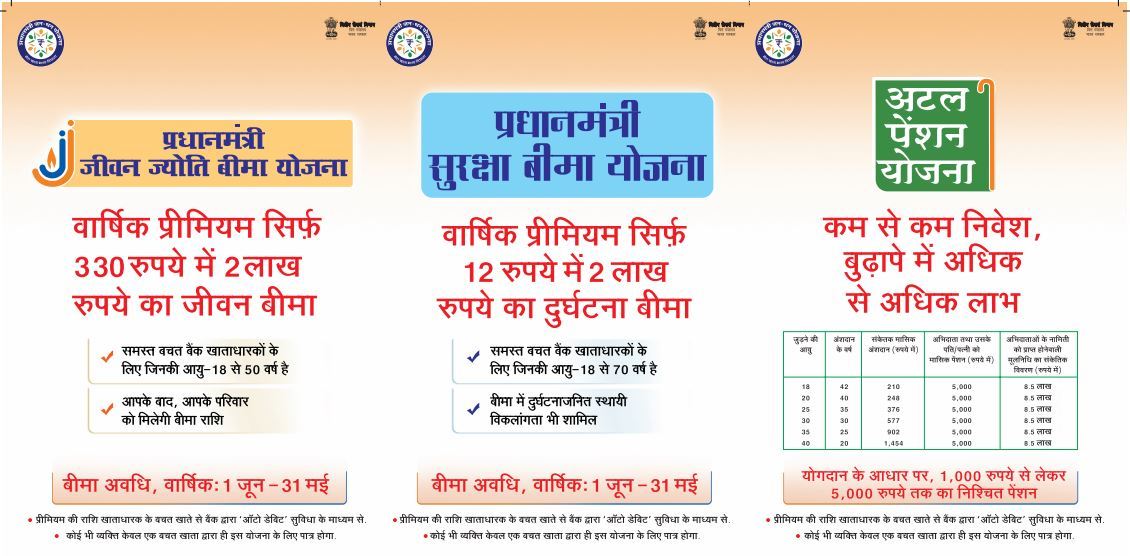

| Eligibility for Other Programs | PMJDY accounts are eligible for Direct Benefit Transfer (DBT), Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJJBY), Pradhan Mantri Suraksha Bima Yojana (PMSBY), and Atal Pension Yojana (APY). |

Successes of PMJDY

- Financial Inclusion: PMJDY is recognized as the largest financial inclusion initiative globally, with over 53 crore bank accounts opened as of August 2024.

- It has facilitated access to credit for individuals without a formal financial history, as evidenced by the rise in Mudra loan sanctions at a compounded annual rate of 9.8% from FY 2019 to FY 2024.

- Social Empowerment: 55.6% of Jan Dhan account holders are women, and 66.6% of accounts are in rural and semi-urban areas, demonstrating the program’s reach among marginalized communities.

- Deposit Growth: The total deposits in PMJDY accounts have reached Rs. 2.31 lakh crore, showing a 15-fold increase since August 2015.

- Digital Transaction Growth: Digital transactions under PMJDY have surged, with UPI financial transactions growing from 535 crore in FY 2018-19 to 13,113 crore in FY 2023-24.

- Effective DBT Mechanism: The Jan-Dhan Aadhaar Mobile (JAM) trinity has enabled a diversion-proof subsidy delivery mechanism, with subsidies and social benefits directly transferred into the bank accounts of the underprivileged.

- Savings and Financial Discipline: The average deposit in the PMJDY account has increased 4 times since August 2015, indicating improved saving habits among account holders.

PYQ:[2015] ‘Pradhan Mantri Jan-Dhan Yojana’ has been launched for (a) Providing housing loan to poor people at cheaper interest rates. (b) Promoting women’s Self-Help Groups in backward areas. (c) Promoting financial inclusion in the country. (d) Providing financial help to the marginalized communities. [2016] Pradhan Mantri Jan Dhan Yojana (PMJDY) is necessary for bringing unbanked to the institutional finance fold. Do you agree with this for financial inclusion of the poorer section of the Indian society? Give arguments to justify your opinion. |

Get an IAS/IPS ranker as your 1: 1 personal mentor for UPSC 2024

Financial Inclusion in India and Its Challenges

India’s Fintech funding plummets amid global slowdown, shows report

From UPSC perspective, the following things are important :

Prelims level: Fintech Sector

Mains level: Challenges and significance of the fintech sector,

Why in the news?

Despite achieving a significant milestone in H1 2024, the fintech sector has encountered notable funding difficulties.

What is the Fintech Sector?

- The fintech sector encompasses technologies and innovations that aim to compete with traditional financial methods in the delivery of financial services. This includes a wide range of applications like mobile banking, online payments, digital lending, and blockchain technology.

Present Report Insights

- Funding Decline: The Indian fintech sector recorded $795 million in funding in H1 2024, a decrease of 11% from H2 2023 and 59% from H1 2023.

- Global Ranking: Despite the decline, the Indian fintech ecosystem ranked among the top three globally funded sectors alongside the US and UK in H1 2024.

- Major Transactions: Only two funding rounds exceeded $100 million in 2024, with Perfios becoming the only unicorn. Bengaluru led the funding, followed by Mumbai and Pune.

- Segment Performance: Alternative Lending, RegTech, and BankingTech were the top-performing segments, with Alternative Lending securing $646 million, making up 81% of the total funding.

- Acquisitions and IPOs: There were six acquisitions and five IPOs in H1 2024, marking significant activity despite the overall funding challenges.

Significance of Fintech Sector

- Financial Inclusion: Fintech innovations enhance financial inclusion by providing access to financial services to unbanked and underbanked populations.

- Economic Growth: The sector contributes significantly to economic growth by fostering innovation, creating jobs, and boosting consumer spending.

- Efficiency and Transparency: Fintech solutions improve efficiency and transparency in financial transactions, reducing costs and fraud.

- Support for Startups: The sector offers numerous opportunities for startups, driving entrepreneurship and competition.

Challenges

- Data Security: Fintech companies must implement strong security measures to protect sensitive customer data from cyber-attacks and data breaches. For example, Acko, a leading Indian fintech startup, has faced issues with data breaches in the past, highlighting the importance of robust data security protocols in the industry.

- Regulatory Compliance: The fintech industry is highly regulated, requiring companies to stay updated on the latest government policies and ensure compliance to avoid penalties. For example, the Reserve Bank of India (RBI) has issued guidelines to protect consumers from predatory lending practices by digital lenders, underscoring the need for fintech firms to navigate the evolving regulatory landscape.

- Customer Acquisition and Retention: Attracting and retaining customers is critical for fintech firms. For example, BharatPe, a prominent Indian fintech company, has faced challenges in customer retention due to its focus on merchant acquisition.

- Funding and Investment: Securing adequate funding and investments remains a challenge for many fintech startups. For example, Paytm, one of India’s largest fintech companies, has faced scrutiny from investors due to its inability to achieve profitability

How India Can Improve Its Fintech Sector

- Supportive Regulatory Environment: Create a regulatory framework that encourages innovation while ensuring consumer protection and systemic stability, facilitating a balanced growth of the fintech ecosystem.

- Infrastructure Development: Invest in digital infrastructure, such as high-speed internet and mobile connectivity, to support the widespread adoption and efficient functioning of fintech applications across the country.

- Focus on Cybersecurity: Ensure robust cybersecurity measures to protect against fraud and cyber-attacks, building trust among users and maintaining the integrity of fintech services.

Steps taken by the government:

|

Conclusion: Fintech companies in India face challenges including data security, regulatory compliance, customer acquisition, and securing investments. Addressing these ensures sustainable growth and trust in a competitive market environment.

Mains PYQ:

Q Has digital illiteracy, particularly in rural areas, coupled with a lack of Information and Communication Technology (ICT) accessibility hindered socio-economic development? Examine with justification. (UPSC IAS/2021)

Get an IAS/IPS ranker as your 1: 1 personal mentor for UPSC 2024

Financial Inclusion in India and Its Challenges

Interest rates on small savings schemes like PPF, SCSS, and NSC are under review by Modi 3.0 government

From UPSC perspective, the following things are important :

Prelims level: Small Savings Schemes

Mains level: Impact of Stable Interest Rates on Small Savings Schemes

Why in the news?

The central government of India is set to announce the interest rates for various small savings schemes, including the Public Provident Fund (PPF), Senior Citizen Savings Scheme (SCSS), National Savings Certificate (NSC), Sukanya Samriddhi Yojana (SSY), and Post Office Monthly Income Scheme (POMIS), for the July-September 2024 quarter by June 30, 2024.

Current Interest Rates and Expected Changes

- Public Provident Fund (PPF)

- Current Rate: 7.1%

- Expected Rate: Despite the benchmark 10-year bond yield averaging 7.02% from March to May 2024, which would suggest a rate of 7.27% according to the formula, experts believe the government will likely maintain the status quo.

- Reason: Factors such as controlled inflation, stable 10-year G-Sec yields, and historical precedence of the government not strictly following the recommended formula indicate a low probability of rate hikes.

2. Senior Citizen Savings Scheme (SCSS)

- Current Rate: 8.2%

- Expected Rate: Unlikely to see significant changes.

- Reason: With a spread of 100 basis points, the SCSS offers a substantial return, and experts predict the government will maintain existing rates to manage fiscal policies effectively.

3. Sukanya Samriddhi Yojana (SSY)

- Current Rate: 8.0%

- Expected Rate: Expected to remain stable.

- Reason: The SSY enjoys a spread of 75 basis points. Given the controlled inflation and fiscal policies, a rate hike is not anticipated.

Factors Influencing Interest Rates

- Benchmark Yields: The interest rates for small savings schemes are linked to the yields of 10-year government securities.

- Market Conditions: Prevailing market yields and inflation rates play a crucial role in determining these rates.

- Government Policy: The central government’s fiscal strategy and policies, such as those outlined in the Union Budget, impact decisions on interest rates.

Impact of Stable Interest Rates on Small Savings Schemes

- Investor Sentiment and Returns

-

- PPF: Investors in PPF may feel disappointed due to the stagnation in interest rates despite a slight uptick in benchmark yields. However, PPF still offers tax-free returns under the Exempt-Exempt-Exempt (EEE) status, making it an attractive long-term investment.

- SCSS and SSY: Stability in interest rates ensures a predictable income stream for senior citizens and parents of girl children, maintaining their trust in these schemes.

- Government Fiscal Management: Maintaining the current interest rates helps the government manage its fiscal deficit more effectively. Higher rates would increase the interest burden on the government, especially for widely subscribed schemes like PPF.

- Inflation Control: Stable interest rates reflect the government’s confidence in managing inflation. By not increasing rates, the government signals that it sees inflation as under control, thus aiming to keep borrowing costs stable for both the government and the public.

- Market Stability: Consistent interest rates contribute to market stability. Predictable returns on small savings schemes help in the planning of household finances, ensuring steady savings and investments. This stability can also foster overall economic stability by maintaining consumer confidence.

Conclusion: Investors in PPF, SCSS, and SSY should prepare for the possibility that interest rates will remain unchanged for the July-September 2024 quarter. While the formula indicates room for an increase in PPF rates, historical trends and expert opinions suggest that the government may maintain the current rates to balance fiscal control and market stability.

Mains PYQ:

Q Pradhan Mantri Jan-Dhan Yojana (PMJDY) is necessary for bringing the unbanked to the institutional fiancé fold. Do you agree with this for the financial inclusion of the poorer section of the Indian society? Give arguments to justify your opinion. (UPSC IAS/2016)

Get an IAS/IPS ranker as your 1: 1 personal mentor for UPSC 2024

Financial Inclusion in India and Its Challenges

India’s Fintech Landscape: Challenges and Recommendations

From UPSC perspective, the following things are important :

Prelims level: Fintech and their regulations

Mains level: Need for regulating Fintechs

Introduction

- The Standing Committee on Communications and Information Technology recently highlighted concerns regarding the dominance of foreign-owned fintech apps in India’s digital payment ecosystem.

- While UPI commands a significant share of digital payments in terms of volume, its value share remains relatively low, raising questions about the distribution and control of digital payment platforms.

What are Fintech?

- Fintech Definition: Fintech, a fusion of “financial” and “technology,” denotes businesses leveraging technology to enhance or automate financial services.

- Types of Fintech Companies: They encompass payment solutions (e.g., Bharatpe), lending platforms (e.g., CRED), insurance providers (e.g., Digit Insurance), investment platforms (e.g., Zerodha), and regulatory technology firms (e.g., Razorpay).

Regulatory Framework in India

- Regulatory Landscape: While direct RBI intervention in regulating fintech companies remains limited, initiatives like the Fin-Tech Regulatory Sandbox and Payment System Operators license aim to embrace and regulate aspects of the fintech sector.

- Future Regulatory Outlook: The RBI is developing a regulatory framework to support orderly growth in digital lending, emphasizing that lending activities should be conducted only by entities regulated by the central bank or under other applicable laws.

Why discuss Fintech?

- India is amongst the fastest growing Fintech markets in the world. Indian FinTech industry’s market size is $50 Bn in 2021 and is estimated at ~$150 Bn by 2025.

- The Indian Fintech industry’s total addressable market is estimated to be $1.3 Tn by 2025 and Assets Under Management & Revenue to be $1 Tn and $ 200 Bn by 2030, respectively

Analysis of Existing Ecosystem

- Regulatory Oversight: The Committee stresses the need for effective regulation of digital payment apps, noting the rising trend of digital transactions in India. It suggests that regulatory bodies like RBI and NPCI would find it more feasible to regulate local apps compared to foreign entities.

- Dominance of Foreign Fintech: Foreign-owned fintech companies, such as PhonePe and Google Pay, dominate the Indian market, commanding significant market shares in terms of transaction volume. In contrast, NPCI’s BHIM UPI holds a minimal market share.

- Regulatory Measures: The NPCI previously imposed a 30% volume cap on transactions facilitated through UPI by third-party apps to maintain market equilibrium and address risks. Compliance timelines were extended to December 2024 to facilitate market growth.

Concerns about Fraud

- Money Laundering: The Committee observed instances of fintech platforms being used for money laundering, citing examples like the Abu Dhabi-based app, Pyppl, administered by Chinese investment scamsters. This poses challenges for law enforcement agencies in tracking illegal money trails.

- Fraud Trends: Despite the rise in digital transactions, the fraud to sales ratio has remained relatively low. However, concerns persist regarding UPI frauds affecting a small percentage of users.

Impact on the Ecosystem

- Advantages of Local Players: Local fintech players possess a natural advantage in understanding customer needs and the broader market infrastructure. Foreign fintechs, on the other hand, bring in expertise in new technologies and global connectivity.

- Revenue Growth: McKinsey’s Global Payments Report suggests that instant payments, including UPI, may contribute less than 10% of future revenue growth due to minimal transaction fees. However, the shift towards digital payments enhances security and access to commerce channels, offsetting the costs associated with managing cash transactions.

Conclusion

- Balancing the dominance of foreign-owned fintech platforms with the promotion of local players is essential for the sustainable growth of India’s digital payment ecosystem.

- Effective regulation, along with efforts to combat fraud and promote financial inclusion, will be crucial in shaping the future trajectory of digital payments in the country.

Get an IAS/IPS ranker as your 1: 1 personal mentor for UPSC 2024

Financial Inclusion in India and Its Challenges

Surge in Farm Loan Disbursals

From UPSC perspective, the following things are important :

Prelims level: Kisan Credit Card (KCC) Scheme

Mains level: Farm Loan

Introduction

- In the first nine months of the current fiscal year, farm loan disbursals have exceeded 90 percent of the Budget estimate, prompting expectations of a significant hike in the Interim Budget for the next fiscal year (2024-25).

- Finance Minister had set a target of ₹20 lakh crore for agriculture credit during the previous fiscal year (2023-24).

Budget Promises and Performance

- Credit Target Increase: Finance Minister Sitharaman had announced an agriculture credit target of ₹20 lakh crore for FY 2023-24. The current disbursement data indicates that this target is likely to be exceeded.

- Sectoral Focus: The Ministry reported that credit disbursed to the Animal Husbandry and Fisheries sector in FY 2023-24 reached ₹1,91,412 crore, constituting 65 percent of the ₹2.93 lakh crore target.

- Working Capital and Term Loans: Disbursements included over ₹77,000 crore as working capital and over ₹1.13 lakh crore as term loans.

Kisan Credit Card (KCC) Scheme Impact

- Significant Growth: Agricultural credit has witnessed substantial growth from ₹7.3 lakh crore in FY 2013-14 to ₹21.55 lakh crore in FY 2022-23, driven by the success of the KCC scheme.

- Operative KCC Accounts: The KCC scheme, facilitating timely and hassle-free credit, boasts over 7.36 crore operative accounts as of the end of 2023.

- Interest Subvention: Concessional interest rates, with a 7 percent lending rate and a 1.5 percent per annum interest subvention, were offered for short-term crop and allied activity loans up to ₹3 lakh through KCC.

About Kisan Credit Card (KCC) Scheme

| Details | |

| Objective | To provide timely and flexible credit support to farmers for various agricultural and related needs. |

| Launch | Introduced in 1998 to issue KCC to farmers, facilitating the purchase of agricultural inputs and cash withdrawals for production needs. |

| Credit Support |

|

| Implementing Agencies | Commercial Banks, Regional Rural Banks (RRBs), Small Finance Banks, and Cooperatives. |

| Eligible Farmers |

|

| Maximum Permissible Limit (MPL) | The short-term loan limit for the 5th year, plus the estimated long-term loan requirement, determines the KCC limit. |

Regulatory Framework and Initiatives

- RBI Mandate: RBI mandates a priority sector lending target for banks, with a specific allocation of 18 percent for agriculture and a 10 percent sub-target for Small and Marginal Farmers (SMFs) for FY 2023-24.

- Prompt Repayment Incentive (PRI): An additional 3 percent PRI is provided for prompt and timely repayment, effectively reducing the interest rate to 4 percent per annum.

- Collateral-Free Agriculture Loans: RBI is set to raise the limit for collateral-free agriculture loans to ₹1.6 lakh from ₹1 lakh, aiming to enhance the coverage of small and marginal farmers.

- Streamlined Lending Practices: Banks have streamlined lending by eliminating ‘no dues’ certificates for small loans up to ₹50,000 and accepting alternative documentation or affidavits for loans to specific categories of farmers.

Financial Inclusion and NABARD Initiatives

- Joint Liability Groups (JLGs): NABARD’s creation of ‘Joint Liability Groups’ has facilitated lending without collateral to tenant/landless farmers and non-farm workers, fostering trust between banks and JLG members.

- JLGs Performance: By March 31, 2023, a total of 257.9 lakh JLGs had been formed and linked to credit, contributing to the broader financial inclusion agenda.

Conclusion

- The surge in farm loan disbursals indicates the success of various government initiatives, particularly the KCC scheme, in promoting financial inclusion and supporting the agricultural sector.

- The likely increase in the agriculture credit target in the upcoming Interim Budget underscores the continued commitment to rural financing and development.

Get an IAS/IPS ranker as your 1: 1 personal mentor for UPSC 2024

Financial Inclusion in India and Its Challenges

Progress track: PM Jan Dhan Yojana’s Milestones

From UPSC perspective, the following things are important :

Prelims level: PM Jan Dhan Yojana

Mains level: Financial Inclusion

Central Idea

- As the PM Jan Dhan Yojana (PMJDY) completes 9 years, its remarkable journey is marked by over 50 crore bank accounts and deposits exceeding ₹2 lakh crore.

- The scheme’s success lies in its commitment to financial inclusion, creating avenues for underprivileged segments to access banking services and government schemes.

What is PM Jan Dhan Yojana (PMJDY)?

- The PMJDY is a financial inclusion program launched by the Indian government in 2014.

- It is National Mission for Financial Inclusion to ensure access to financial services, namely, a basic savings & deposit accounts, remittance, credit, insurance, pension in an affordable manner.

- Under the scheme, a basic savings bank deposit (BSBD) account can be opened in any bank branch or Business Correspondent (Bank Mitra) outlet, by persons not having any other account.

Benefits under PMJDY

- One basic savings bank account is opened for unbanked person.

- There is no requirement to maintain any minimum balance in PMJDY accounts.

- Interest is earned on the deposit in PMJDY accounts.

- Rupay Debit card is provided to the account holder.

- Accident Insurance Cover of Rs.1 lakh (enhanced to Rs. 2 lakh to new PMJDY accounts opened after 28.8.2018) is available with RuPay card issued to the PMJDY account holders.

- An overdraft (OD) facility up to Rs. 10,000 to eligible account holders is available.

Is PMJDY a success?

- Dormancy of accounts: The PMJDY scheme has led to an increase in the number of bank accounts in rural areas. The percentage of zero-balance accounts has significantly decreased from 58% in March 2015 to a mere 8%, indicating a more active engagement with banking services.

- Low or no transactions: Insurance coverage for the account holder is linked to their transaction history, and many accounts remain frozen due to lack of transactions, taking several weeks or months to reactivate.

- False promise of overdraft: The promised overdraft facility of Rs 5000 for new account holders has not been provided as promised, leading to scepticism about the scheme’s success.

- Payments bottleneck: The lack of proper connectivity, electricity, internet, and ATM facilities in rural areas has hindered the activation of RuPay cards and PIN numbers, which should have been considered before implementing such a large-scale program.

Future prospects

- Voluntary Participation: The government aims to persuade PMJDY account holders to opt for voluntary micro-insurance schemes like PMJJBY and Pradhan Mantri Suraksha Bima Yojana.

- Persuasion over Compulsion: The focus is on financial literacy campaigns, special drives, and awareness programs conducted by banks to help account holders make informed choices.

- Multi-Level Coordination: Collaboration with line ministries, including Anganwadi and Asha workers, enhances awareness campaigns and ensures wider coverage.

- Leveraging Databases: Utilization of databases like the E-Shram portal for labour-related information aids in identifying potential beneficiaries.

Get an IAS/IPS ranker as your 1: 1 personal mentor for UPSC 2024

Financial Inclusion in India and Its Challenges

National Pension Scheme (NPS)

From UPSC perspective, the following things are important :

Prelims level: National Pension Scheme (NPS)

Mains level: Not Much

Central Idea

- The Pension Fund Regulatory and Development Authority (PFRDA) has introduced a new feature for systematic withdrawal from the National Pension Scheme (NPS).

National Pension Scheme (NPS): A Brief Overview

- The National Pension Scheme (NPS) is a voluntary retirement savings scheme launched by the Government of India in 2004.

- It is regulated and administered by the Pension Fund Regulatory and Development Authority (PFRDA).

- The primary objective of the NPS is to provide a pension income to individuals upon their retirement.

Key Features of the NPS:

- Contributions: Subscribers make regular contributions to their NPS account during their working years. These contributions accumulate and grow over time.

- Investment Options: The NPS offers two investment options: a) Auto Choice: where the funds are invested based on the subscriber’s age, and b) Active Choice: where the subscriber can select the asset classes (equity, corporate bonds, and government securities) and the fund manager.

- Portable Account: The NPS account is portable, allowing subscribers to maintain their account even if they change jobs or locations.

- Withdrawal Options: Upon retirement, subscribers have the flexibility to withdraw a portion of their accumulated corpus as a lump sum and use the remaining amount to purchase an annuity, which provides a regular pension income.

- Tax Benefits: NPS offers tax benefits at different stages. Contributions made by subscribers are eligible for tax deductions under Section 80C, while withdrawals are subject to certain tax exemptions.

- Regulated and Transparent: The NPS is regulated by the PFRDA, ensuring transparency and oversight of the scheme. It follows strict investment guidelines and has mechanisms in place to safeguard the interests of subscribers.

- Wide Coverage: The NPS is available to all Indian citizens, including salaried employees, self-employed individuals, and non-resident Indians (NRIs).

Benefits of the NPS

- Retirement Income: The NPS provides a retirement income to subscribers, ensuring financial security during their post-retirement years.

- Long-term Wealth Creation: The investment component of the NPS allows subscribers to accumulate wealth over time, potentially generating higher returns and building a substantial retirement corpus.

- Flexibility and Control: Subscribers have the flexibility to choose their investment options and actively manage their NPS accounts, providing a level of control over their retirement savings.

- Tax Efficiency: The NPS offers tax benefits both on contributions and withdrawals, making it a tax-efficient retirement savings option.

- Portability: The portability feature of the NPS allows subscribers to continue their account irrespective of job changes or relocations.

- Regulated and Secure: The NPS is regulated by the PFRDA, ensuring a secure and transparent framework for retirement savings.

Changes introduced: Systematic Withdrawal Plan

- NPS subscribers will be allowed to withdraw 60% of their contributions systematically post-retirement.

- The current system of one-time withdrawal will be replaced.

- 40% of the contributions must be in annuity.

- Systematic withdrawals can be customized by the subscriber based on their needs.

- Withdrawals can be made in lump sum or on a monthly, quarterly, half-yearly, or annual basis.

- This feature is applicable to individuals aged 60-75.

Benefits offered by this change

- Flexibility: Subscribers can customize their withdrawals based on their financial needs.

- Regular Income: Systematic withdrawals provide a regular income stream post-retirement.

- Enhanced Financial Planning: Allows for better financial planning and management.

Get an IAS/IPS ranker as your 1: 1 personal mentor for UPSC 2024

Financial Inclusion in India and Its Challenges

IRDAI’s ambitious plan ‘Bima Trinity’

From UPSC perspective, the following things are important :

Prelims level: BIMA Trinity

Mains level: Insurance sector reforms

Central Idea

- The Insurance Regulatory and Development Authority (IRDA) in India aims to implement ambitious plans to improve the insurance sector.

- The key objectives include offering affordable bundled policies that cover multiple risks and providing expedited claim settlements with value-added services.

“Bima Trinity” – A Comprehensive Plan

- The IRDA is collaborating with general and life insurance firms to develop a comprehensive plan called “Bima Trinity.”

- Bima Sugam

- Bima Vistar

- Bima Vaahaks

(1) Bima Sugam – One-Stop Shop Platform

- The IRDA is developing the Bima Sugam platform, which will integrate insurers and distributors onto a single platform.

- This platform will serve as a one-stop shop for customers, simplifying the process of purchasing policies and accessing services.

- Customers will be able to pursue service requests and settle claims through the same portal, enhancing convenience and efficiency.

(2) Bima Vistar

- The IRDA is working on the development of Bima Vistar, a bundled risk cover that encompasses life, health, property, and casualties or accidents.

- This bundled policy aims to provide comprehensive protection against a wide range of risks.

- Policyholders will have defined benefits for each risk, allowing for faster claim payouts without the need for surveyors.

- Bima Vistar will offer defined benefits for each risk category, ensuring clarity and ease of understanding for policyholders.

- If a loss occurs, the defined benefit will be promptly transferred to the policyholder’s bank account, eliminating unnecessary waiting periods.

(3) Bima Vaahaks: Women-Centric Workforce

- As part of the Bima Trinity plan, the IRDA envisions a women-centric workforce known as Bima Vaahaks.

- Bima Vaahaks will operate at the Gram Sabha level and engage with women heads of households.

- Their role will be to educate and convince women about the benefits of a comprehensive insurance product like Bima Vistar.

- They will emphasize the usefulness of a composite insurance product like Bima Vistar during times of distress.

- By highlighting the advantages and addressing concerns, these Bima Vaahaks will play a crucial role in empowering women and ensuring their financial security.

Other developments

- Leveraging Digitized Registries for Faster Claims: With the increasing digitization of birth and death registries in many states, the IRDA plans to integrate its platform with these registries. This integration would allow for seamless sharing of data and facilitate faster claim settlements.

- Streamlined Claim Settlement Process: Policyholders can access the platform, retrieve their policy from the insurers’ repository, and provide the necessary documents, such as the death certificate. This swift claim settlement process revolutionizes the insurance industry by significantly reducing the time taken for policyholders to receive their claims.

Expansion of Insurance Penetration

(1) Legislative Amendments for Increased Investments

- The IRDA plans to introduce legislative amendments to attract more investments into the insurance sector. These amendments would allow for differentiated licenses for niche players, similar to the banking sector.

- The objective is to encourage more participation, ultimately making insurance more accessible and affordable for citizens.

(2) Making Insurance Available, Affordable, and Accessible

- The IRDA is focused on adopting a multi-level approach to make insurance available, affordable, and accessible to a larger population.

- The aim is to address the low insurance penetration in the country and double the number of jobs in the sector.

- The regulator believes that by implementing these changes, insurance can become more inclusive and reach citizens at the Gram Sabha (village council), district, and state levels.

(3) Identifying Significant Protection Gaps

- The IRDA acknowledges the existence of significant protection gaps in various lines of insurance, including life, health, motor, property, and crops.

- These gaps highlight the need for comprehensive coverage and prompt claim settlements.

Proposed Amendments for Regulatory Reforms

The IRDA has proposed amendments to insurance laws to enable regulatory reforms that encourage increased investment and innovation.

- Differentiated capital requirements: These amendments aim to introduce differentiated capital requirements for niche insurers, attracting more investment into the sector.

- Other value-added services: Additionally, the proposed amendments will allow insurers to offer value-added services alongside policies, catering to the evolving needs and preferences of customers.

- Encouraging new players and services: The proposed amendments will pave the way for the entry of new players in the insurance sector. Micro, regional, small, specialized, and composite insurers will have the opportunity to operate and cater to different geographical areas and population segments.

Comparison with Banking Sector

- The IRDA draws parallels between the proposed changes in the insurance sector and the existing diversity in the banking sector.

- Similar to the banking sector, which includes various types of banks addressing different needs and geographies, the insurance sector can benefit from a diverse range of insurers.

- Payment banks, small finance banks, cooperative banks, and other specialized institutions serve specific purposes and cater to distinct segments of the population.

Way Forward

The IRDA’s initiatives, including bundled policies and expedited claim settlements, have the potential to significantly enhance insurance accessibility and affordability in India. To move forward effectively, the following steps can be considered:

- Collaborating with Insurers: The IRDA should work closely with insurance companies to refine and implement the Bima Trinity plan, ensuring the success of bundled policies and integrated platforms.

- Technological Integration: Prioritizing the integration of birth and death registries with the IRDA platform to expedite claim settlements. Emphasizing technological advancements and partnerships for seamless data sharing and processing.

- Awareness and Education: Launch a comprehensive awareness campaign in collaboration with insurers and stakeholders to educate the public, especially women, about the benefits of bundled policies and comprehensive insurance coverage.

- Regulatory Reforms: Expediting proposed amendments to insurance laws to enable differentiated capital requirements and value-added services. Active engagement with relevant government bodies to ensure smooth implementation.

- Monitoring and Evaluation: Establishing a robust framework for monitoring and evaluating the effectiveness of bundled policies, claim settlement processes, and insurance penetration in different regions.

- Continuous Innovation: Encouraging insurers to continuously innovate and develop new products and services that address emerging risks and meet evolving consumer preferences in the rapidly evolving insurance landscape.

Get an IAS/IPS ranker as your personal mentor for UPSC 2024

Get an IAS/IPS ranker as your 1: 1 personal mentor for UPSC 2024

Financial Inclusion in India and Its Challenges

India’s Pension Reforms: Ensuring Pension Security

From UPSC perspective, the following things are important :

Prelims level: OPS, NPS and other alternatives

Mains level: pension system, ensuring security and stability

Central Idea

- The issue of government employees’ pension has emerged as a critical political concern, leading several states to consider reverting from the New Pension Scheme (NPS) to the defined-benefit (DB) Old Pension Scheme (OPS). Acknowledging the significance of this matter, the Government of India has established a committee to enhance the NPS.

What is pension?

- A pension is a retirement plan that provides a stream of income to individuals after they retire from their job or profession. It can be funded by employers, government agencies, or unions and is designed to ensure a steady income during retirement.

What is Old Pension Scheme (OPS)?

- The OPS, also known as the Defined Benefit Pension System, is a pension plan provided by the government for its employees in India.

- Under the OPS, retired government employees receive a fixed monthly pension based on their last drawn salary and years of service.

- This pension is funded by the government and paid out of its current revenues, leading to increased pension liabilities.

What is NPS?

- NPS is a market-linked, defined contribution pension system introduced in India in 2004 as a replacement for the Old Pension Scheme (OPS).

- NPS is designed to provide retirement income to all Indian citizens, including government employees, private sector workers, and self-employed individuals

Facts for prelims: Key differences between the two pension schemes

| Parameters | The Old Pension Scheme(OPS) | The New Pension Scheme (NPS) |

| Nature of the schemes | OPS offer pensions to government employees on the basis of their last drawn salary | NPS pays the employees for their investments in the NPS Scheme during their employment. |

| Amount of pension derived | 50 per cent of the last drawn salary | 60% lump sum after retirement and 40% to be invested in annuities for getting a monthly pension |

| Benefits in taxes | No tax benefits | The employee can claim tax deductions of 1.5 lakh under Section 80C of income tax and up to 50,000 on other investments under 80CCD (1b) |

| Tax on pension | No tax on pension | 60% of the NPS Corpus is tax-free while the remaining 40% is taxable |

| Option of Investment | No option | Two choices: Active and Automatic |

| Who can avail? | Only government employees | Any Indian Citizen between 18-65 years. |

| Switching Schemes | OPS scheme can be switched to NPS | NPS scheme cannot be switched back to OPS in general, but central government employees can switch back to OPS in case of death and disablement of the employee. |

Reasons behind the growing demand for reverting to OPS

- Stability and Predictability: One of the primary motivations for the demand to return to OPS is the desire for stability and predictability in pension benefits. Under the OPS, employees receive a fixed pension based on their last drawn salary, which is increased periodically to account for inflation. This offers a sense of security and certainty about post-retirement income, ensuring a stable financial future.

- Market Risk and Annuity Payouts: The NPS, being a market-linked pension scheme, exposes pensioners to market risks. The returns on the pension fund are subject to market fluctuations, which can impact the overall corpus and subsequently affect annuity payouts. This volatility raises concerns among employees who seek a more secure and reliable pension arrangement.

- Lower Annuity Prospects: With the NPS, pensioners bear the market risk and face the possibility of lower-than-expected annuity amounts. This uncertainty about future pension prospects prompts many employees to advocate for a return to OPS, which offers a predetermined pension amount.

- Comparisons with Other Pension Systems: Employees often compare the OPS with pension systems in other countries, particularly those in the Organisation for Economic Co-operation and Development (OECD) economies. These comparisons reveal that OPS provides higher pension replacement rates, lower retirement ages, and covers the entire family. Such favorable aspects of OPS generate a perception of better benefits and incentivize employees to demand its reinstatement.

- Perception of Unsustainability: While the NPS was introduced to address fiscal strains associated with the unfunded OPS, there are concerns about its long-term sustainability. Some argue that OPS can be sustained through effective fiscal management and reform, rather than completely abandoning it. The perception of unsustainability drives the demand for reverting to OPS as a viable alternative.

Challenges involved in reverting back to OPS

- Fiscal Sustainability: The OPS operates on a pay-as-you-go (PAYG) system, where present workers finance the retired. With declining birth rates and increased life expectancy, the burden on the future workforce to fund pensions will intensify. The OPS, being an unfunded scheme, poses challenges in maintaining fiscal sustainability in the long run.

- Demographic Shifts: The dependency ratio is expected to increase substantially, with fewer workers supporting a larger number of retirees. This demographic shift adds to the challenges of sustaining the OPS, as it puts additional strain on the funding mechanism and the ability to meet pension obligations.

- Inflationary Pressures: The OPS guarantees periodic increases in pension payouts through dearness allowance (DA) adjustments to account for inflation. However, relying on fixed increments tied to DA can pose challenges during periods of high inflation. Ensuring that pension payments keep pace with inflation without compromising fiscal stability can be a complex task for policymakers.

- Budgetary Constraints: The financial burden of reverting to OPS can put a significant strain on the government’s budget. Pension liabilities already account for a substantial portion of states’ revenue receipts and own revenues. Increasing pension obligations may lead to a reduction in development expenditure or necessitate additional borrowing, potentially exacerbating the issue of public debt.

- Inter-generational Equity: Maintaining inter-generational equity is a crucial consideration in pension reforms. Reverting to OPS might fulfill the aspirations of current employees, but it can impose a heavy burden on future generations. Striking a balance between providing reasonable pension security for present employees and ensuring the sustainability of the pension system for future generations is a key challenge that needs to be addressed.

- Economic Factors: The economic environment, including interest rates and investment returns, can impact the financial viability of OPS. Changes in economic conditions, such as low interest rates or inadequate returns on pension fund investments, can strain the financial resources needed to sustain OPS and meet pension obligations.

Way ahead: Building sustainable and inclusive pension systems

- Comprehensive Reform: Governments should undertake comprehensive reforms which may involve revisiting the pension architecture, introducing alternative pension models, and exploring hybrid schemes that combine elements of defined-benefit and defined-contribution systems. Reforms should be guided by a thorough analysis of demographic trends, fiscal constraints, and economic conditions.

- Adequate Funding Mechanisms: Pension systems must establish robust funding mechanisms to ensure that pension obligations can be met. This may involve setting up dedicated pension funds, implementing sound investment strategies, and establishing appropriate contribution rates for both employees and employers.

- Strengthening Pension Governance: Effective governance is crucial for the success of pension systems. Governments should strengthen the regulatory framework, improve transparency, and enhance accountability in the management of pension funds. Establishing independent oversight bodies and adopting international best practices can help ensure the integrity and efficiency of pension governance.

- Promoting Financial Literacy: Financial literacy programs should be implemented to educate individuals about the importance of retirement planning, investment strategies, and the risks and benefits associated with different pension options. Empowering individuals with financial knowledge will enable them to make informed decisions and take an active role in securing their retirement income.

- Encouraging Voluntary Savings: Governments should encourage voluntary retirement savings programs to complement the mandatory pension schemes. Providing incentives, such as tax benefits or matching contributions, can incentivize individuals to save for retirement beyond the mandatory contributions. Voluntary savings options, such as individual retirement accounts or employer-sponsored plans, can offer individuals greater flexibility and control over their retirement savings.

- Flexibility and Portability: Pension systems should adapt to the changing nature of work and support individuals with diverse employment patterns. Portable pension accounts that allow individuals to carry their accumulated benefits across jobs can ensure continuity of retirement savings. Flexibility in pension payout options, such as lump sum withdrawals or phased withdrawals, can accommodate different financial needs and preferences of retirees.

- Social Safety Nets: To address the needs of vulnerable populations, social safety nets should be incorporated into pension systems. These safety nets can provide minimum income guarantees or targeted assistance for individuals with limited or interrupted work histories, low-income earners, and those facing economic hardships in retirement.

Conclusion

- Amidst the debate between NPS and OPS, it is crucial to devise a pension system that ensures security without compromising fiscal sustainability and inter-generational equity.

Must read:

| Contributory Guaranteed Pension Scheme (CGPS): A Considerable Alternative |

Get an IAS/IPS ranker as your 1: 1 personal mentor for UPSC 2024

Financial Inclusion in India and Its Challenges

Contributory Guaranteed Pension Scheme (CGPS): A Considerable Alternative

From UPSC perspective, the following things are important :

Prelims level: OPS, NPS and CGPS

Mains level: Contributory Guaranteed Pension Scheme (CGPS) Analysis

Central Idea

- The debate on pensions is heating up as several state governments announce their reversion to the old pension scheme (OPS). However, economists have frowned upon this move, citing two major reasons. Firstly, since the state has to bear the full burden of pensions, it may become fiscally unsustainable in the long run. Secondly, an unsustainable rise in pension allocation in the budget can come at the cost of other welfare expenditures allocated to the poor and marginalized sections.

What is mean by pension?

- A pension is a retirement plan that provides a stream of income to individuals after they retire from their job or profession. It can be funded by employers, government agencies, or unions and is designed to ensure a steady income during retirement.

What is Old Pension Scheme (OPS)?

- The OPS, also known as the Defined Benefit Pension System, is a pension plan provided by the government for its employees in India.

- Under the OPS, retired government employees receive a fixed monthly pension based on their last drawn salary and years of service.

- This pension is funded by the government and paid out of its current revenues, leading to increased pension liabilities.

What is the National Pension System (NPS)?

- The Union government under PM Vajpayee took a decision in 2003 to discontinue the old pension scheme and introduced the NPS.

- The scheme is applicable to all new recruits joining the Central Government service (except armed forces) from April 1, 2004.

- On the introduction of NPS, the Central Civil Services (Pension) Rules, 1972 was amended.

What are two arguments against reverting to the old pension scheme?

- Fiscal Unsustainability: Since the State has to bear the full burden of pensions, it will become fiscally unsustainable in the medium to long run.

- Trade-Off with Welfare Expenditure: Such an unsustainable rise in pension allocation in the Budget can only come at the cost of other more pressing welfare expenditures allocated to the poor and marginalized sections.

The commonality between the two arguments

- Both arguments assume that the fiscal revenues are fixed, which is not necessarily the case if the government has its priorities right.

- Both arguments assume that unsustainable rise in pension allocation in the Budget can only come at the cost of other more pressing welfare expenditures allocated to the poor and marginalized sections.

Why Public sector workers are asking for a guaranteed pension in place of the NPS?

- Fluctuating pension returns: The NPS is market-based, which means that the pension returns fluctuate according to the returns prevailing in the market. This creates uncertainty and makes it difficult for employees to plan for their post-retirement life.

- Guaranteed pension: Public sector workers are looking for a guaranteed pension that will provide them with a fixed amount after retirement. This will ensure a stable and predictable post-retirement life for them.

- Employee contribution: In the new contributory guaranteed pension scheme (CGPS), a large part of the pension will be funded by the employees themselves. This is in contrast to the old pension scheme (OPS) where no contribution was required from the employees.

- Protection against market fluctuations: The CGPS provides protection to employees against market fluctuations. If the market return happens to be higher than the guaranteed pension, the State gets to pocket the difference. On balance, the additional burden on the CGPS may be marginal compared to the NPS.

- Burden-sharing: The CGPS ensures that the burden of uncertainty does not fall on employees alone. In the OPS, elite workers gain at the cost of their brethren lower on the income ladder. However, in the CGPS, the burden is only the employer’s contribution part, exactly as in the NPS.

Potential disadvantages of a CGPS

- Higher contribution burden on employees: Under the CGPS, employees will continue to contribute a fixed percentage of their basic pay towards their pension. This may put a higher burden on them compared to the current system, where their contribution fluctuates based on market returns.

- Additional administrative burden: Implementing a new pension scheme like CGPS may involve additional administrative burden and costs for the government, which could be challenging to manage efficiently.

- Uncertainty of market returns: While the CGPS guarantees a fixed pension amount, it does not provide any certainty on the market returns. If the market returns are lower than expected, the government will have to bear the burden of paying the difference between the guaranteed pension and the actual pension.

Facts for prelims: CGPS vs NPS

| Parameter | Contributory Guaranteed Pension Scheme (CGPS) | National Pension scheme (NPS) |

| Type of Scheme | Guaranteed Pension Scheme | Market-linked Pension Scheme |

| Contributions | Made by both employee and employer | Made by the employee only |

| Pension Amount | Guaranteed 50% of the last drawn salary, adjusted for inflation | Market-linked, varies according to returns |

| Risk | Risk is shared by both employee and employer | Risk is borne entirely by the employee |

| Burden on exchequer | Burden is only on the employer’s contribution part | Burden is on the entire pension amount |

| Upside | State gets to pocket the excess if the market return is higher | No upside for the State |

| Fiscal sustainability | Can be sustainable with proper rationalisation of taxes | Unsustainable in the medium to long run |

Way ahead

- The government could consider implementing the Contributory Guaranteed Pension Scheme (CGPS) as an alternative to the New Pension Scheme (NPS) for public sector workers.

- The CGPS would allow the state to pocket any excess returns from the market, rather than bearing the entire burden of uncertain market returns as in the NPS.

- The government should consider rationalizing taxes, such as implementing inheritance and wealth taxes, to increase its revenue and reduce its dependence on fixed fiscal revenues.

- The government should set up a special task force to rationalize pensions and address the issue of pension sustainability in the long run.

- A possible downside to the CGPS is that it may require a higher contribution from employees, which could affect their take-home pay during their working life. However, this could be addressed by offering tax breaks or other incentives to encourage employees to contribute to the scheme.

Conclusion

- The current debate on pensions in India has brought forth the need for a well-designed and sustainable pension scheme that can cater to the needs of public sector workers while being fiscally responsible. The CGPS presents a viable alternative to the OPS and the NPS providing public sector workers with a guaranteed pension after they retire while also being largely funded by the employees themselves. While there may be some challenges in implementing the CGPS, with proper planning and execution, the CGPS could serve as a model for sustainable and equitable pension schemes that can support the growing needs of an ageing workforce in India.

Mains question

Q. The debate on pensions is heating up as several state governments announce their reversion to the old pension scheme. Do you think Contributory Guaranteed Pension Scheme (CGPS) presents a viable alternative to the OPS and the NPS?

Also read:

| Reversal To Old Pension Scheme (OPS): Potential Impact |

Get an IAS/IPS ranker as your 1: 1 personal mentor for UPSC 2024

Financial Inclusion in India and Its Challenges

Only half PMJDY insurance claims settled in 2 years

Central idea: In an RTI reply, it is revealed that only 329 claims out of 647 filed were settled in the last two financial years under the Pradhan Mantri Jan Dhan Yojana (PMJDY).

What is PM Jan Dhan Yojana (PMJDY)?

- The PMJDY is a financial inclusion program launched by the Indian government in 2014.

- It is National Mission for Financial Inclusion to ensure access to financial services, namely, a basic savings & deposit accounts, remittance, credit, insurance, pension in an affordable manner.

- Under the scheme, a basic savings bank deposit (BSBD) account can be opened in any bank branch or Business Correspondent (Bank Mitra) outlet, by persons not having any other account.

Benefits under PMJDY

- One basic savings bank account is opened for unbanked person.

- There is no requirement to maintain any minimum balance in PMJDY accounts.

- Interest is earned on the deposit in PMJDY accounts.

- Rupay Debit card is provided to the account holder.

- Accident Insurance Cover of Rs.1 lakh (enhanced to Rs. 2 lakh to new PMJDY accounts opened after 28.8.2018) is available with RuPay card issued to the PMJDY account holders.

- An overdraft (OD) facility up to Rs. 10,000 to eligible account holders is available.

Why in news?

- In the financial year 2021-22, 341 claims were received for accident insurance cover under the PMJDY scheme.

- Out of these, 182 claims were settled and 48 were rejected.

- No information was provided on the status of the remaining 111 claims.

Is PMJDY a success?

- Dormancy of accounts: The PMJDY scheme has led to an increase in the number of bank accounts in rural areas, but this has not necessarily led to a corresponding increase in transactions due to limited transaction history of many account holders.

- Low or no transactions: Insurance coverage for the account holder is linked to their transaction history, and many accounts remain frozen due to lack of transactions, taking several weeks or months to reactivate.

- False promise of overdraft: The promised overdraft facility of Rs 5000 for new account holders has not been provided as promised, leading to scepticism about the scheme’s success.

- Payments bottleneck: The lack of proper connectivity, electricity, internet, and ATM facilities in rural areas has hindered the activation of RuPay cards and PIN numbers, which should have been considered before implementing such a large-scale program.

Get an IAS/IPS ranker as your 1: 1 personal mentor for UPSC 2024

Financial Inclusion in India and Its Challenges

Reversal To Old Pension Scheme (OPS): Potential Impact

From UPSC perspective, the following things are important :

Prelims level: Overview of various pension schemes

Mains level: Issues with OPS and NPS

Central Idea

- The New Pension Scheme (NPS) implemented by the NDA government in 2003-04 was a far-sighted reform that moved towards a sustainable contributory pension system. However, some state governments have reversed the pension reform and returned to the financially burdensome and fiscally non-viable Old Pension Scheme (OPS).

What is pension?

- A pension is a retirement plan that provides a stream of income to individuals after they retire from their job or profession. It can be funded by employers, government agencies, or unions and is designed to ensure a steady income during retirement.

What is OPS?

- The OPS, also known as the Defined Benefit Pension System, is a pension plan provided by the government for its employees in India.

- Under the OPS, retired government employees receive a fixed monthly pension based on their last drawn salary and years of service.

- This pension is funded by the government and paid out of its current revenues, leading to increased pension liabilities.

What is NPS?

- NPS is a market-linked, defined contribution pension system introduced in India in 2004 as a replacement for the Old Pension Scheme (OPS).

- NPS is designed to provide retirement income to all Indian citizens, including government employees, private sector workers, and self-employed individuals.

Negative impacts of the reversal to OPS

- The reversal to OPS would have negative impacts, especially on the poor and vulnerable population, including women and children. Here are some potential impacts:

- Reallocation of resources: The reversal to OPS would lead to a reallocation of resources away from the state’s development expenditure, which benefits the poor, and towards a much smaller group of people who have benefited from a secured and privileged job throughout their working life. It could worsen inequality and lower economic growth in the states.

- Reduction in productivity: Going back to OPS would reduce the productivity of the poor, further diminishing their future economic prospects. Economic services such as infrastructure and rural and urban development would be affected more severely than social services.

- Fiscal burden: The old pension scheme (OPS) was financially burdensome and fiscally non-viable. As public employees’ life expectancy increased, the state’s fiscal burden under the OPS began to rise exponentially, necessitating pension reforms. Reversing to OPS would put the fiscal burden back on the government, which could have negative impacts on the state’s finances.

- Tradeoff between pensions and development expenditure: Pension reforms were a watershed moment for the states, and reversing to OPS would result in a tradeoff between pension and development expenditure of the states. The pension reforms aimed to finance the increased non-development expenditure related to pensions through taxes or borrowing. However, our analysis revealed that from 1990 to 2004, the states’ revenues did not match the state’s increased expenditure, resulting in a higher fiscal deficit.

Facts for prelims: NPS vs OPS

| Parameter | National Pension System (NPS) | Old Pension Scheme (OPS) |

| Type of System | Defined Contribution System | Defined Benefit System |

| Funding | Contributions from employee and employer | Government-funded |

| Investment | Market-linked investments in various asset classes | No direct investment involved |

| Returns | Subject to market risks | Predetermined and not market-linked |

| Pension Amount | Depends on accumulated corpus and investment returns | Based on last drawn salary and years of service |

| Annuity & Lump-sum Withdrawal | Minimum 40% corpus used to purchase annuity, remaining can be withdrawn as lump-sum | Fixed monthly pension, no annuity or lump-sum withdrawal |

| Portability | Portable across jobs and sectors | Limited to government employees |

| Flexibility | Choice of investment options, fund managers, and asset allocation | No flexibility, pension determined by predefined formula |

Conclusion

- The state governments should not ignore the impact of the OPS on the poor and vulnerable, particularly women and children. The reversal will deprive them of essential services such as health and education and prevent them from participating in growth opportunities. Therefore, state governments should not reverse the far-sighted pension reform and should continue to focus on development expenditure that benefits the poor.

Mains Question

Q. What is the New Pension Scheme (NPS) and how does it differ from Old Pension Scheme (OPS) Now states are reversing to OPS as a populist measure, discuss its the negative impacts.

Get an IAS/IPS ranker as your 1: 1 personal mentor for UPSC 2024

Financial Inclusion in India and Its Challenges

Old Pension Scheme (OPS): A Call for Equitable Distribution of Resources

From UPSC perspective, the following things are important :

Prelims level: NPS

Mains level: Pension reforms and challenges

Central Idea

- The demand for the old pension scheme (OPS) is growing in India, particularly after some states announced plans to revert to it. The mainstream critique of OPS is centered around inefficiency and fiscal deficit concerns. However, it is crucial to examine the policy from the class and welfare perspectives.

What is pension?

- A pension is a retirement plan that provides a stream of income to individuals after they retire from their job or profession. It can be funded by employers, government agencies, or unions and is designed to ensure a steady income during retirement.

What is Old Pension Scheme (OPS)?

- The OPS, also known as the Defined Benefit Pension System, is a pension plan provided by the government for its employees in India.

- Under the OPS, retired government employees receive a fixed monthly pension based on their last drawn salary and years of service.

- This pension is funded by the government and paid out of its current revenues, leading to increased pension liabilities.

Did you know: The National Pension System (NPS)?

- NPS is a market-linked, defined contribution pension system introduced in India in 2004 as a replacement for the Old Pension Scheme (OPS).

- NPS is designed to provide retirement income to all Indian citizens, including government employees, private sector workers, and self-employed individuals.

Analyzing the Impact of OPS on India’s Socio-Economic Landscape

- Inequality and Regressive Redistribution: Under the National Pension System (NPS), the Sixth Pay Commission increased the basic salary of government employees to cover pension contributions and promote post-retirement savings. As a result, the salary of a government employee is higher than the income of more than 90% of the population. The OPS thus acts as a regressive redistribution mechanism favoring a better-off class.

- Rising Pension Liabilities: Pension liabilities of the government increased substantially due to the Sixth pay matrix, reaching 9% of total state expenditure. By 2050, pension expenditure will account for 19.4% of total state expenditures, assuming the current growth rate remains constant.